⚡ Key Takeaways

- 1.Inflation is the Enemy: FD returns (approx 7%) barely beat inflation (6%), meaning your purchasing power stays flat.

- 2.Tax Efficiency: SIP gains are taxed at 12.5% (LTCG), while FD interest is taxed at your slab rate (up to 30%).

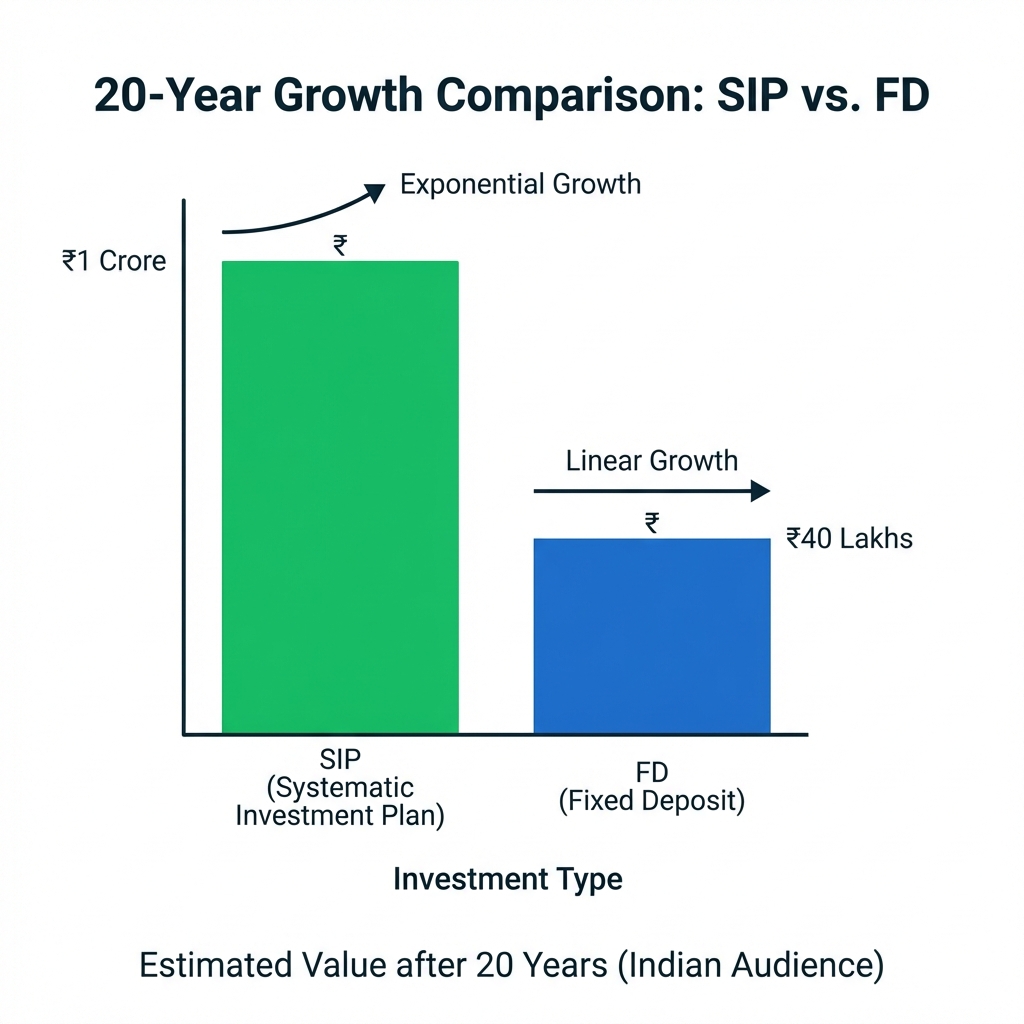

- 3.The Wealth Gap: Over 20 years, a SIP can generate 2x to 3x more wealth than an FD due to compounding.

For generations, Indian families have trusted the Fixed Deposit (FD) as the ultimate safety net. "Put your money in the bank and forget it" was the golden rule passed down from fathers to sons. But in 2025, adhering blindly to this advice might be the biggest risk to your financial future.

While FDs offer capital safety, they suffer from a silent killer: Inflation risk. In this guide, we break down the math of why Systematic Investment Plans (SIP) in equity mutual funds are necessary for any goal more than 5 years away, such as retirement or a child's education.

Why This Analysis Matters

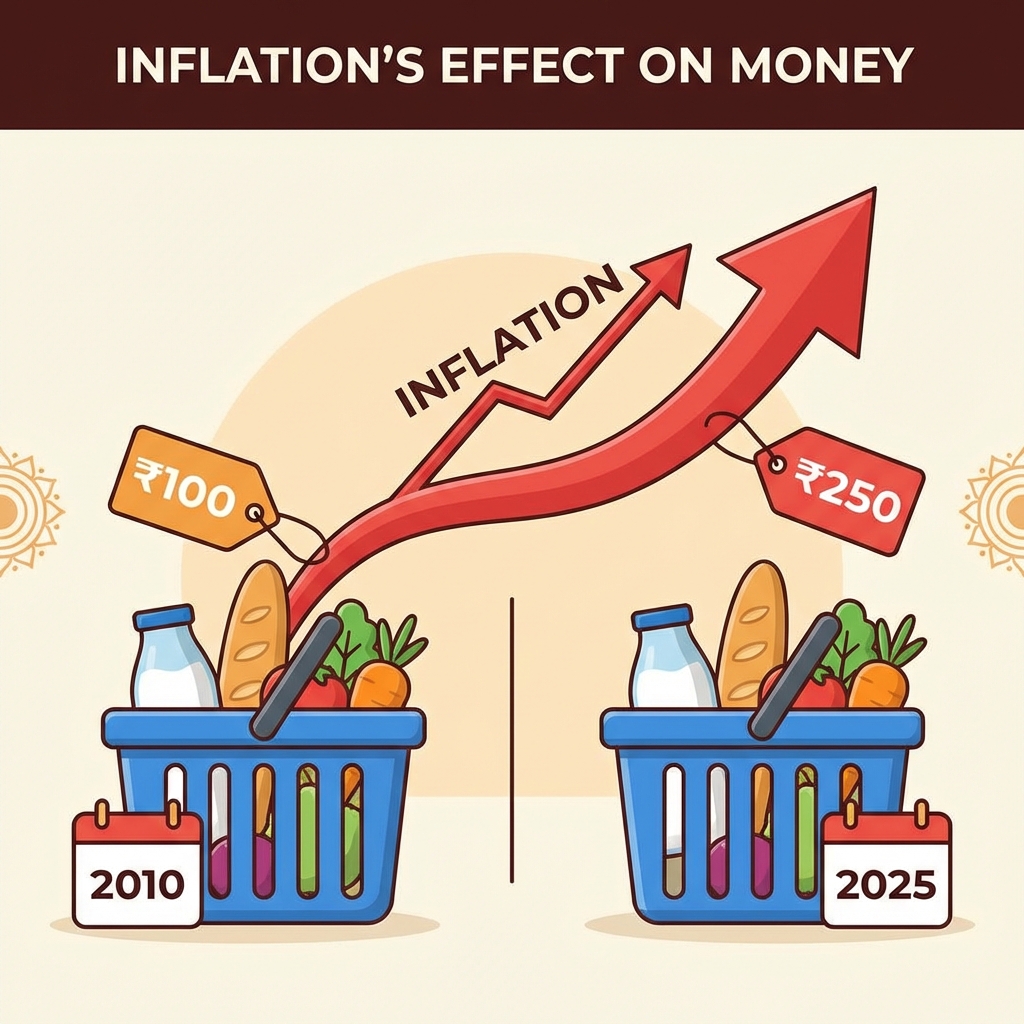

The Reserve Bank of India (RBI) targets an inflation rate of 4% (+/- 2%), but real lifestyle inflation (education, healthcare) often exceeds 8-10%. If your investments aren't beating this number by a wide margin, you are effectively becoming poorer every year.

1. The Mathematics of "Real Returns"

When a bank offers you 7.5% interest per annum, it feels secure. But you must look at the Real Rate of Return.

The Formula:Real Return = Interest Rate - Inflation Rate

If inflation is at 6% (standard long-term average in India) and your FD gives 7%, your real growth is only 1%. It would take 72 years to double your purchasing power at this rate!

In contrast, the Nifty 50 (India's stock market index) has historically delivered 12-14% returns over 15-year periods. Even after removing 6% inflation, you are left with a 6-8% real gain. This is the difference between "saving money" and "building wealth".

2. The Taxation Trap (FD vs SIP)

Many investors ignore taxation. FDs are taxed as per your income slab.

| Parameter | Fixed Deposit (FD) | Equity Mutual Fund (SIP) |

|---|---|---|

| Tax Basis | Taxed as Income (Up to 30%) | Capital Gains (LTCG) |

| Rate | 30% (Highest Slab) | 12.5% (Above ₹1.25L profit) |

| Effective Return (After Tax) | ~4.9% | ~11.5% |

The Verdict: If you are in the highest tax bracket, FDs barely cover inflation post-tax. SIPs remain highly tax-efficient.

3. The Power of Compounding (Real Scenario)

Let's verify this with a real-life example. Suppose Rahul and Priya both save ₹10,000 per month for 20 years.

- Rahul chooses a "Safe" Bank FD at 6% interest.

- Priya starts a SIP in an Index Fund expecting 12% returns.

The Results after 20 Years:

- Total Invested: ₹24 Lakhs (Both)

- Rahul's Corpus (FD): ~ ₹46 Lakhs

- Priya's Corpus (SIP): ~ ₹99.9 Lakhs

Priya has more than double the wealth of Rahul, simply by choosing the right asset class. This is the power of compounding working at a higher rate.

Don't believe the math?

Run the numbers yourself. Adjust the return rate and see how just 2% extra can change your life.

Open SIP Calculator NowFrequently Asked Questions

Common queries answered for you

No, FD is capital-protected (safer), while SIP is market-linked. However, over long periods (10+ years), diversified Equity SIPs have historically beaten inflation and FDs by a significant margin.

Yes. Compounding works best over time. Investing ₹10,000/month for 20 years at 12% returns can yield approx ₹1 Crore, whereas an FD at 6% would yield only around ₹46 Lakhs.

Yes, but they are tax-efficient. Long Term Capital Gains (LTCG) above ₹1.25 Lakh/year are taxed at 12.5%. FDs are taxed at your income slab rate (up to 30%+), making them less efficient for high earners.

Disclaimer

This content is provided for educational and informational purposes only. It does not constitute financial, investment, or legal advice. Calculations are based on historical data and assumed rates of return. Market investments are subject to risk. Financial decisions should be made based on individual circumstances and, where appropriate, in consultation with a qualified professional.